I had a lightbulb Doh! moment yesterday: there is an eerily close rhyme between the evolution of the coffee industry and the evolution of the consulting industry. Like coffee, consulting is entering its fourth wave. Even the dates line up fairly well. Here is a graphic laying out the analogy in detail. For those of you unfamiliar with the 4 coffee waves, I’ll briefly explain that (it’s a great story) and elaborate on the mapping.

The Four Waves of Coffee

Pre-industrial coffee was some mix of global luxury commodity, like spices, and local artisan markets where there was supply within cheap local reach. Then 4 waves played out, each wave creating its own kind of customer.

-

In the first wave, coffee grew from a limited market to a huge, global mass market, thanks to industry consolidation, reliable commodity supply chains, and the rise of large mass-market brands of cheap blended coffee, like Folgers and Nescafe. Coffee became a domestic staple everywhere, like tea before it.

-

In the second wave, brands like Starbucks created a premium retail coffee industry globally, a market for differentiated blends/flavors, globalized differentiated supply chains, and an early-stage single-origin market. They also created a lot of flashy, faddish products, and signaled more quality than they actually delivered in the base product. The also created an experience economy around coffee: a scaled-up version of the Viennese coffee house, and fueled growing aversion towards the low-quality first-wave product.

-

In the third wave, a wave of independent coffee shops (often with their own roasting and sourcing operations) took advantage of the globalized, high-visibility supply chains created by the second wave, and more advanced artisanal brewing technologies, to create a connoisseur’s market based on single-origin beans and careful brewing. They created an educated consumer sensitive to terroir and suspicious of faddishness. Many connoisseurs became home-brew experts as well. Many baristas ran coffee appreciation and brewing classes, making the industry more like the wine industry. Starbucks tried to join the third-wave market with its Reserve and Roastery outlets, with limited success.

-

In the fourth wave, the curated indie cafe experience turned into newer high-end chains with values-based brand promises, like Stumptown, Blue Bottle, Verve, and Intelligentsia. These chains cultivated both their own high-end coffee experiences, and sold premium roasted beans for home-brewers. The artisanal brewing methods evolved into more of a mix of science and art. The fourth-wave outlets are unabashedly ideological, with strong politics on display in the business model, gleefully overwrought mission statements, art-gallery level attention to aesthetics, and highly visible secondary charitable missions.

The big takeaway here is that each wave created its own class of customer for coffee, adapted to the capabilities of the wave. Individual businesses couldn’t really fight this. The dynamics were bigger than them. A couple of quirky anecdotes reveal the nuances of this story.

First there is the story of the Clover, an extremely high-end $11,000 brewing machine that was effectively positioned as an AI barista, able to finely control brew temperatures and times customized to beans. It arrived in the middle of the third wave, and was quickly acquired by Starbucks. But it never quite made an impact. Some think Starbucks bought it to kill it, but I believe it was the right machine at the wrong time, at the wrong price point, rather like the Segway. A little too early, and with an element of thoughtless over-engineering, a bit like the Juicero. As many commentators pointed out at the time of the acquisition, the output of the $11,000 machine could be replicated by a skilled barista using pour-over equipment worth $200. All you really needed was a temperature-controlled kettle, a hand-cranked burr grinder, a decent ceramic filter, and good filter paper.

Second, there is the Nespresso. During this period, Nestle went after the home/office automatic brewing machine market. Previously you either had crappy drip coffeemakers or high-end espresso rigs. K-cup machines occupied the uneasy middle: apparent ability to handle different blends and beans, but not really. Nespresso machines on the other hand, with their bar-coded custom capsules and smarter brew control, did change the game. I bought a Nespresso Vertuoline (now Vertuo) when it first came out around 2013, and have been using it daily for 7 years. During that period, I also got pretty good at pour over at home. They are not directly comparable (Nespresso machines basically produce espresso and dilute it into Americanos for drip-coffee sizes), but of similar quality.

The Clover failed to challenge the fundamentally artisan orientation of the third wave. I suspect an equivalent could be made for under $1000 today, and have much more success within the fourth wave (for example, in franchisee locations of brands like Verve or Stumptown). The Nespresso machines succeeded in finessing a part of the discerning consumer demand for artisanal coffee into a proprietary, vertically integrated coffee-machine/capsule market (it’s possible, but quite hard, to hack Nespresso machines by refilling your own used capsules).

The takeaways from these 2 anecdotes is: you cannot really fight the really big megatrends, but you can time things right, and finesse the trends on the margins. What drove the four-wave history of retail coffee was simply globalization, growing business and technical knowledge, improving equipment, and better quality control.

Now let’s apply the story template to consulting.

The Four Waves of Consulting

Pre-industrial consulting was basically advice from Robber Barons in their memoirs, and local business savvy supplied by Rich Uncles. Then four waves played out.

-

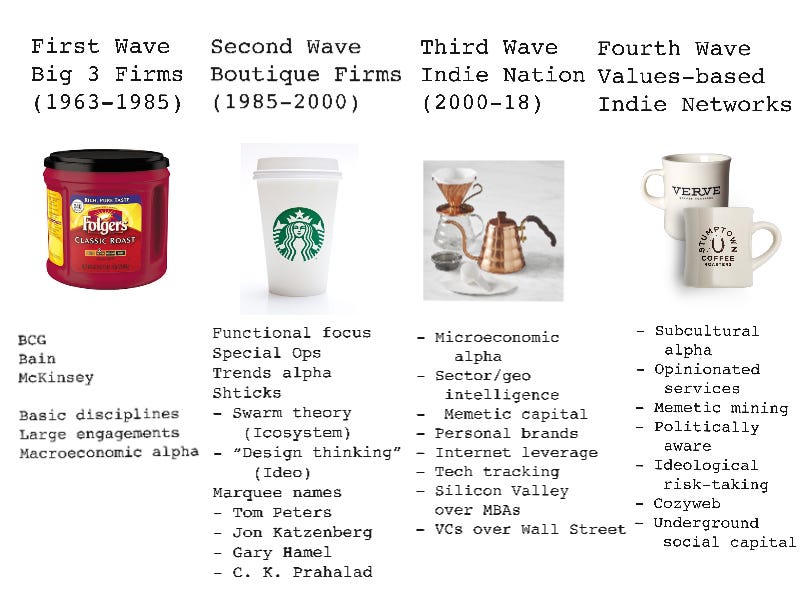

In the first wave, starting with BCG in 1963, as the world slowly started getting off the highly planned, regulated, and protectionist path and into globalized competition, consulting became a meaningful activity. It accelerated with the oil shocks and Japanese competitive threat of the seventies, and came into its own with deregulation in 1980. BCG, Bain, and McKinsey dominated the game, with support from “positioning school” management academics like Michael Porter, who came from an economics background. The Big 3 tended to focus on the very basic “Folgers” grade corporate-wide strategy functions: restructuring, layoffs, efficiency/productivity.

-

In the second wave, starting in the late 80s with small boutique firms headed up by marquee-name thought leaders (often heretic-alumni of the Big 3) like Tom Peters, Jon Katzenbach and others, consulting acquired a big secondary market of premium customers. As with wine and coffee connoisseurs, there was a lot more signaling than taste cultivation going on, and frequently, faddish and shticky value propositions based on esoteric theories du jour, like chaos theory, “design thinking” or “systems thinking.” The idea that consulting is about “flavor of the month” offerings can be blamed squarely on the second wave, just as Frappuccinofication of coffee can be blamed on Starbucks. As with Frappuccinos, boutique firms often peddled sugary coffee-flavored desserts as coffee. They favored flashy thought leadership, airport bestseller writing, and keynoting. Just as Frappuccinos are great as dessert but not as coffee, second-wave consulting output is great as entertainment but not as consulting advice. But there was also genuine movement away from CYA consulting in service of 80s deregulatory playbooks, and towards real curiosity about management as an art and science one could get better at.

-

In the third wave, powered by the internet and blogging, around 2000, a wave of indie consultants hit the market. Like their barista counterparts, indies were unconstrained either by economies of scale or by the reliance on marquee-name airport-bestseller rainmaking. Using small, online personal brands and networks, they were able to find and cultivate a clientele for their fundamentally bespoke, high-trust offerings. Though the third wave had its share of second-wave style faddishness (*cough* lean startup *cough* four-hour anything), most indies tended to play a longer, more self-effacing game, developing substantial offerings over 4-5 years of trial-and-error practice rather than flashy ones piloted as a TEDx Podunk talk, and hastily repackaged into a book. They moved away from both first-wave cynical CYA consulting and second-wave theatrics, and towards genuine business nerdery as a calling. But the price was a sharp limit on scale. Like the early third wave coffee shops, they tended to be too dependent on founder-baristas and struggled to open even a second location.

-

In the fourth wave, which is just over two years old, the indie world is transitioning from individual business nerdery and personal brands/networks to more of a science, and creating a landscape dominated by shared networks rather than individual indie consultants. The Yak Collective is one such network that I’ve helped instigate, one with a focus on pragmatism and delivery, and devoted to consulting as something of an empirical science you can study and get better at through trial and error. There are others with different shared values. For example, I just read this NYT article about an emerging network/subculture of indie consultants devoted to spiritual counseling. I hate every element of this particular example, but the point is, the fourth wave is made up of varied subcultures of indies with shared values.

It’s really early days yet with the fourth wave, both for coffee and consulting. But there’s definitely something going on.

Waves and Generations

At the risk of over-simplifying this, for both coffee and consulting you could say:

-

First wave is the Silent Generation with a cronyist ethos and no taste.

-

Second wave is Boomers with a flashy charisma ethos, some taste, and a lot of stagecraft.

-

Third wave is Gen X with a retreating/self-effacing nerd ethos and skeptical but deeply held tastes. It’s obviously the best wave.

-

Fourth wave is Millennials with an ironic/kayfabe ethos and cynically performative tastes.

This shouldn’t be too surprising. Both coffee and consulting are products for minds. Psychoactive products that link to producer and consumer personalities. You should expect to see echoes of generational personalities. Both are also mid-career markets. Your coffee tastes settle down around when you settle down into an adult career.

You typically land in indie consulting in mid-career too. By age 30-35, you know how you like your coffee, and have enough work experience to be fuel a consulting career.

That said, this is just a fun aside. Don’t take the generational mapping too seriously.

Third-Wave Blues

I’m a pretty stereotypical and representative third-waver myself, I’m frankly suspicious of a lot of the things the fourth wave seems to stand for. This means I occasionally suffer what I call the third-wave blues witnessing the rise of the fourth wave and the slow passing of the third. What I dislike about the fourth wave:

-

It’s more uncritically communal than I like

-

It’s more theatrically ideological and political than I like

-

It vastly over-indexes on aesthetics and appearances

-

There is a certain self-importance to it

There’s a clear third-wave/fourth-wave generational tension. If third-wavers were trial-and-error consulting nerds, fourth-wavers are consulting auteurs who have Theories about How the World Should Work, and expect to arrive on the scene with ideological documents, and be listened to.

Still, on some fronts, it feels like the Fourth Wavers are onto real doctrinal discoveries and innovations that perhaps the empirically wired “show me” Gen X third-wavers are too skeptical of. I try to watch out for this tendency too much skepticism in myself. My general approach to mitigating this risk is sometimes betting against my own instincts, and on the instincts of younger people. They might not have logged the hours of experience I have, but they might be attuned to weak signals in the environment I’m deaf to. They can log the experience over time, but my attunement is only likely to get worse. So it’s time for me to listen despite my suspicions and instinctive dislikes.

To some extent, I’m probably going to stay stuck in the third wave for the rest of my career. I’m 45, and a bit set in my ways. That said, I’m open to many elements of the fourth wave, which is part of why I’m devoting significant bandwidth to the Yak Collective experiment, which is definitely a very fourth-wave thing. In some ways, I’m too old by about a decade to be part of that kind of experiment, but in other ways, I’m enough of a business and consulting nerd to want to learn from it.

Will the fourth wave grow up and disrupt the first three waves significantly? Will it stumble and fail? Will I grow into it, or stay stuck in my third-wave niche?

You can ask these questions about both coffee and consulting. I suspect the answers are actually going to be the same.

***

This has been one of the occasional free issues of the Art of Gig newsletter. In the four weeks since the last free issue (July 30th: Leverage Curves and Career Paths), I published the following subscriber-only issues:

-

August 6th: The Art of Being Unmanaged

-

August 13th: The Prosumer Gambit

-

August 19th: Dog-Fooding for Indies

-

August 27th: Reality-Arbitrage vs. Dog-Fooding

For those who signed up recently, Art of Gig is a weekly newsletter on the gig economy, with a particular focus on indie consulting. I typically do a free issue at least once a month.